Imagine a company in which there are no controls at all. It’s hard to believe… Nevertheless, employees who have to set up an internal control system often have the feeling that they are starting from a blank page.

And yet, as a general rule, almost 90% of the controls already exist. The implementation of internal control simply allows the formalization of these controls and the creation of a framework conducive to their proper implementation. Once in place, the system is regularly reviewed in order to highlight some weaknesses and identify other controls or monitoring. You will then have a more efficient internal control and reduce risks.

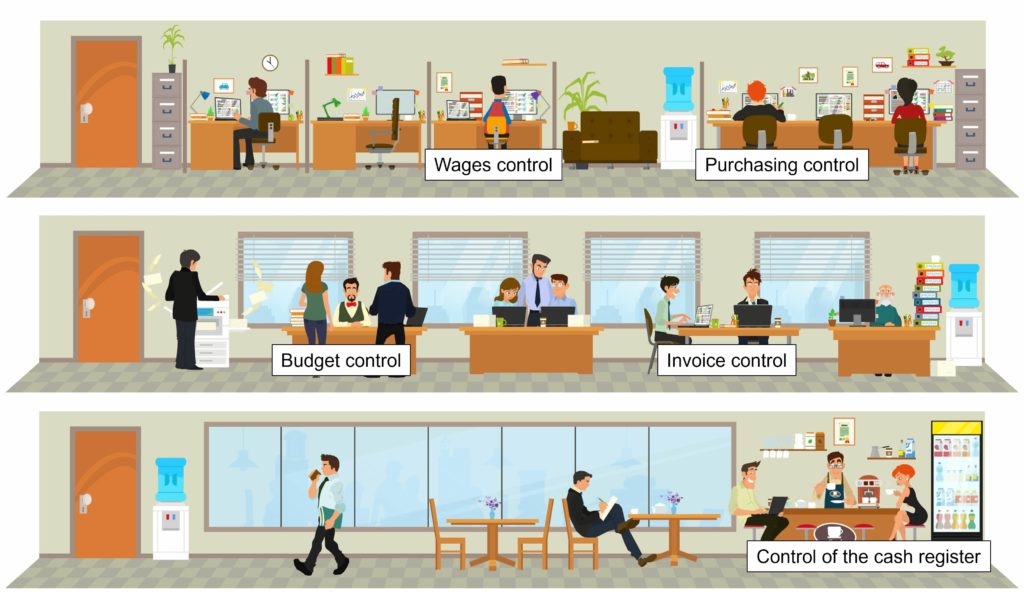

Here is a series of 7 controls that are likely to exist in your organization and that can be easily formalized to start implementing your internal control.

1- Control of purchasing needs

Safeguards are in place to prevent purchases that do not meet the company’s needs or fraudulent purchases made for personal needs.

For example, a control of the merits of the purchase by the department manager is a first protection. Another example is to control the budget to ensure that the purchase is within the defined framework and does not exceed the budget.

2- Control of supplier invoices

Upon receipt of an invoice, it is usually to check that it is justified. The following elements are checked: wording, quantity, amount, reality of the service, etc.

3- Control of wages

Although the extent and method of control can vary greatly, a control of wages before they are paid is generally performed. Whether it is based on the salary journal or on the provisional salary slips, the amounts are checked by a person other than the one who issued the documents.

4- Control of cash

To avoid discrepancies between cash and accounting balances, counting coins and bills is the most effective way to verify that they match. If carried out at the right frequency, this control makes it easy to correct any discrepancies or to quickly highlight any problems.

5- Control of insurance statements

In order to ensure that the reimbursements correspond to the contractual conditions, a control of the statement data upon receipt is usually carried out.

6- Control of cash flow

A regular control, for example weekly, of the cash flow is useful to ensure that the institution has sufficient liquidity to support its future expenses.

7- Control of budget

Similarly, regular control of the budget situation is essential to avoid the possibility of overspending at a later date. Depending on the results of the control, the company’s financial strategy can be readjusted: making unplanned investments, restricting expenses, etc.

In summary, internal control practices – often unconscious – are already an integral part of companies’ day-to-day operations. Using internal control software such as Optimiso Suite allows these controls to be formalized and automated, thereby strengthening efficiency and compliance.